")

Many of the homeowners whose retirement age is approaching often are in need of additional funds. The extra money can be used for home renovation , line of credit for emergency, and multiple other use cases dependent on the unique financial situation of the users. A reverse mortgage is a way for older people with an age bracket greater than 62 to borrow money that is based on the equity of their home. Here’s what you need to know in detail about the potential risks, working, best deals and much more. Let’s dive into the basic details of the reverse mortgage.

Table of Contents

What is reverse mortgage?

everse mortgage like all the other traditional loans allow the homeowners to borrow money while using their home as a security of the loan. Homeowners who are above the age bracket of 62 and has considerable home equity can borrow money against the value of their home. The money you receive is in lump sum with fixed monthly payments or line of credit.

It is important to mention here that its does not work the same way as all other home loans. When you take a reverse mortgage loan, the title of your home remains in your name. Unlike all the traditional mortgage in the reverse mortgage loan the borrowers don’t make monthly payments. The loan is repaid in the way that when the borrower dies and ultimately moves out of the home.

In this type of loan, the interest rates and fees are added to the loan balance every month and the balance grows. If you get a reverse mortgage loan, you still have to pay all the property taxes and other home insurance and should keep the home in good condition.

Key Considerations

- Reverse mortgage is the type of loan for people that are above the age of 62

- This type of loan lets the homeowners to easily convert the home equity into cash income with no fixed monthly payments

- As each person has a distinct financial situation so taking a reverse mortgage loan is a great financial decision for some people while poor financial decision for the others

- It is crucial to understand the working of reverse mortgage and how they will impact your family in the future

Details of reverse mortgage

The good aspect of the reverse mortgage is that you don’t have to make loan payment your life time. But importantly the Federal regulations require homeowners to structure the payments in a way that the amount of loan don’t exceed the price of your current home.

How does reverse mortgage work?

The reverse mortgage loan is taken against the equity that the principal property has incurred. The equity is converted into cash that the lender will give to the borrower in lump sum. Like the regular mortgage this also has interest charges applied. For instance as many borrower take money as lump sum amount so the interest rate is charged on the whole amount.

While same goes for the other borrowers if they choose monthly payments or line of credit, the interest rates are applicable to the money they receive not the entire balance. Also, the unused funds that are part of the line of credit accrue interest. The greatest difference is how the loan is paid back to the lender. The entire balance is due when you are no longer the primary resident of the home in two conditions when the homeowner decides to sell the home or when the homeowner dies.

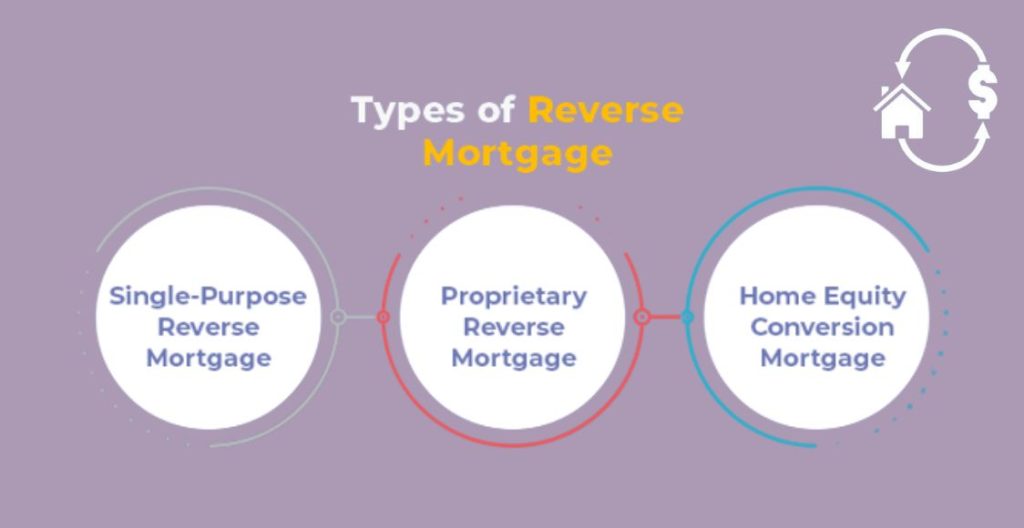

What types of reverse mortgage are there?

It is a common perception that the reverse mortgages are considered as the best last resort. If you are loan that is government-insured and prefer loan without federal insurance than reverse mortgage loan is the viable choice .

Standard Home Equity Conversion Mortgages (HECM)

This one is the most popular reverse mortgage that is backed by the U.S Department of Housing and Urban Development and Federal Housing Administration. This type of loan is available both with an adjustable rate and fixed rate.

- The fixed rate option is only available in case of lump sum payment by the lender to the borrower. This can favor the borrower to lock the mortgage when the interest rates are low.

- The adjustable rate is better known for flexible terms and conditions. As with adjustable-rate loan the borrower has the option to set a fixed monthly disbursement amount based. The line of credit can also be increased depending on the incurred interest rates and will not be canceled like the Home Equity Line of Credit

Single Purpose Reverse mortgages

Not all the reverse mortgage loans are federally insured some are also backed up by government agencies. These types of loans are offered by non-profit organizations and other state-governed agencies that can only be used for particular purposes that include paying property taxes and repairing the home. As smaller amount of equity is used so this can lower the overall cost .

If you are in search on single-purpose reverse mortgage lenders then research for the local agencies in your area that provide home repair loans. This loaning scheme is the least expensive option in reverse mortgage loans.

Proprietary Reverse Mortgage

For the homeowners that have high-value properties, the federally set borrowing limit may feel restrictive. To support the homeowners with a property that is greater than the value of $1,089,300, jumbo proprietary reverse mortgage is a good option. This type of loaning scheme is usually backed up by the private bank to facilitate a specified user base. As they are not insured by FHA therefore it does not require the insurance premium along with all specific requirements of the HECM. It is important to mention here that the interest rates are typically higher than the standard home equity conversion mortgages.

If you have decided to opt for the option of a reverse mortgage consider the following three options in detail to finalize one viable approach for yourself.

Payment processing for Reverse Mortgages

There are several ways you can choose to receive the proceeds in one of the six ways including the following:

- Lump sum – This way you get all the proceeds at once when your loan closes. This is the only option with fixed interest rates

- Equal monthly payments – As long as you have one borrower living in the principal residence the loan giver will make steady payments to the borrower. This one is also regarded as the tenure plan.

- Line of credit – Considering the home equity, the money is made available to the borrower as needed. The interest rate is charged on the money you take out from the particular credit line.

- Term payments – The loan lenders offer borrowers a schedule for equal monthly payments for a set period of time particularly 10 years or more

- Equal monthly payments and line of credit – With steady monthly payments for as long as one borrower is the principal resident, the borrower can easily get more money at any point of time with access to line of credit

- Term payments and line of credit – The lender gives the borrower the money for a specific time frame such as 10 years and in case the borrower needs more money, he can access it from the line of credit.

What documents are necessary to apply for reverse mortgage?

The documents that are necessary for the approval of reverse mortgage include the following :

| Document Name | Description |

| Proof of Age | A valid government-issued ID, such as a driver’s license or passport, to verify that you are at least 62 years old. |

| Proof of Homeownership | A copy of your deed or mortgage statement to prove that you own the home you want to use for the reverse mortgage. |

| Proof of Income | Recent pay stubs, tax returns, or Social Security award letters to show that you have enough income to pay your property taxes and homeowners insurance. |

| Home Appraisal | A professional appraisal to determine the current market value of your home. |

| Credit Report | A recent credit report to assess your creditworthiness. |

| Proof of Counseling | A certificate of completion from a HUD-approved counseling session to verify that you understand the terms and conditions of a reverse mortgage. |

| Property Tax Bill | A copy of your most recent property tax bill to show that you are up to date on your property taxes. |

| Homeowners Insurance Policy | A copy of your current homeowners insurance policy to verify that you have adequate coverage for your home. |

Can reverse mortgage interest be deducted?

Yes it can be in some cases . As you improve the home you may be able to receive deduced interest rates. But if you use the proceeds for other payments such as medical billing and other big expenses than the interest rate will stay the same. Here are few requirements to lower the interest rates on reverse mortgages.

- For interest deductions it is important to itemize your deductions on your federal tax return.

- You must use the proceeds to buy, build or improve your home. Once you renovate your home you can potentially decrease the interest rates.

Who should get a reverse mortgage?

The reverse mortgage loan may sound similar to a home equity line of credit but its different from HELOC . As per the market value of your home you are eligible to get a lump sum of money or the line of credit to use it gradually . Unlike the HELOC you don’t need to have good to excellent credit score and stable income to qualify for this loaning scheme. Unless and until you have the primary residence, you can easily qualify for reverse mortgages. This is the only option for senior citizen who wants to access the home equity without selling the home for those :

- Who don’t want the responsibility of making monthly loan payment

- Who are enable to qualify for HELOC due to low credit score or limited cashflow.

- Who cannot afford to make monthly loan payments?

However, there are other approaches that can grant you lump sum of money but all of them want monthly repayment.

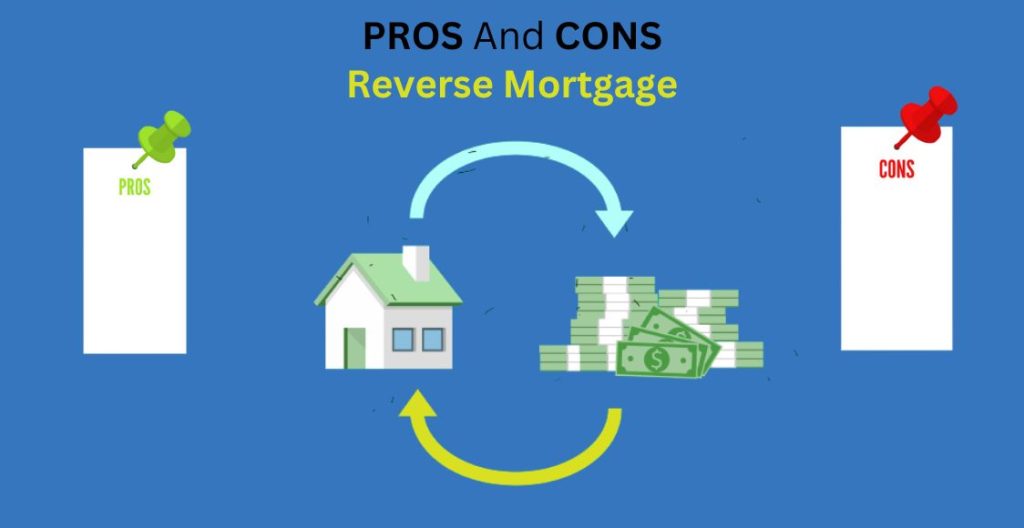

Pros and Cons of Reverse Mortgage

The pros and cons for reverse mortgage is listed in the form of the table below :

| Pros | Cons |

| Reverse mortgages allow you to access a portion of the equity you’ve built up in your home without having to pay taxes on the money you receive. This can be a valuable source of income for retirees who are on a fixed budget. | As you borrow money against your home equity with a reverse mortgage, the amount you owe on your home increases. This can leave your heirs with a smaller inheritance if you sell your home or pass away. |

| With this type of mortgage, you are bound to pay monthly mortgage payments. This can free up your cash flow and make it easier to afford your living expenses in retirement. | There are upfront costs associated with getting a reverse mortgage, such as origination fees, closing costs, and mortgage insurance premiums. These costs cos may vary but its typically several thousand dollars |

| A reverse mortgage can help you stay in your home for as long as you want to. This can be especially beneficial if you have strong ties to your community or if you have family and friends nearby. | As you borrow money against your home equity with a reverse mortgage, the amount of equity you have in your home decreases. This can make it more difficult to sell your home in the future. |

| Unlike traditional mortgages, reverse mortgages do not require you to have good credit to qualify. This can be a good option for seniors who have had some financial setbacks in the past. | If you sell your home or pass away, your heirs may inherit a home with less equity than they would have if you had not taken out a reverse mortgage. |

Interest Rates on Reverse Mortgages

Only the lump sum money option for reverse mortgages charges a fixed interest rate. The other options have adjustable interest rates that may change with the passage of time. The variable interest rate is tied to the benchmark index, constant maturity treasury index, and various other factors. Few of the lenders add a margin of 0.1-0.5 to the borrowers. But the good aspect is that the credit score have no impact on the interest rates of reverse mortgages.

When do you have to repay the reverse mortgage?

The lender will require the borrower to repay the reverse mortgage in one of the following cases :

- If the borrower sells the home the loan lender immediately demands the money

- If the borrower fail to maintain the house then he has to immediately return the money back to the lender

- If the borrower resides out of the principal residence then he have to pay the reverse mortgage loan on urgent basis

- If the borrower is not able to pay homeowners insurance premiums and other property taxes

Also, there are few other exceptions in case the spouses want to stay in the home if their partner passes away.

How you can avoid scams related to reverse mortgages?

Although scammers have different approaches to stealing money and looting you. But there are certain factors you should keep in consideration

- Contractor scams

Beware of all the contractors that approach you to get reverse mortgage loan. Although not all of them are fraud but don’t put yourself in pressure of getting a reverse mortgage loan.

- Other scams

As the Department of Veterans Affair does not offer any kind of reverse mortgage loans , so it is important to be aware of the false claims. Few of the mortgage ads usually states veterans special offers and another no-payment reverse mortgage to grab the attention of Older Americans.

Who owns the house in the reverse mortgage?

The borrower of the mortgage loan owns the house. The good aspect of this loaning scheme is that you keep the title of the home and maintain its complete ownership. This means that you are entirely responsible for all the property taxes, home insurance, repairs, and other such expenses.

Read More

Frequently Asked Questions

What are three different types of reverse mortgages?

The three different types of reverse mortgage loans are following:

1. Standard Home Equity Conversion Mortgages (HECM)

2. Single Purpose Reverse mortgages

3. Proprietary Reverse Mortgage

What is the 95% rule on the reverse mortgage?

In case the loan balance is more than the total value of the home, then it’s likely that the state will sell the home for at least 95% of the value and the lenders will accept the payment as the repayment of the loan.

Who guarantees the reverse mortgage?

The Federal Housing Administration guarantees the reverse mortgages. FHA is part of the Department Housing and Urban Development that insures Standard Home Equity Conversion Mortgages in which your house was taken as security to lend you the loan money.

{kind=link}